In 2008, an anonymous author using the name Satoshi Nakamoto published a short paper that introduced Bitcoin — and with it, a new idea: a shared record of events that can be trusted without trusting any single owner.

The core question is simple: how can many independent participants agree on “what happened” when there is no central database, no administrator, and no single party in charge?

In One Minute

What to remember

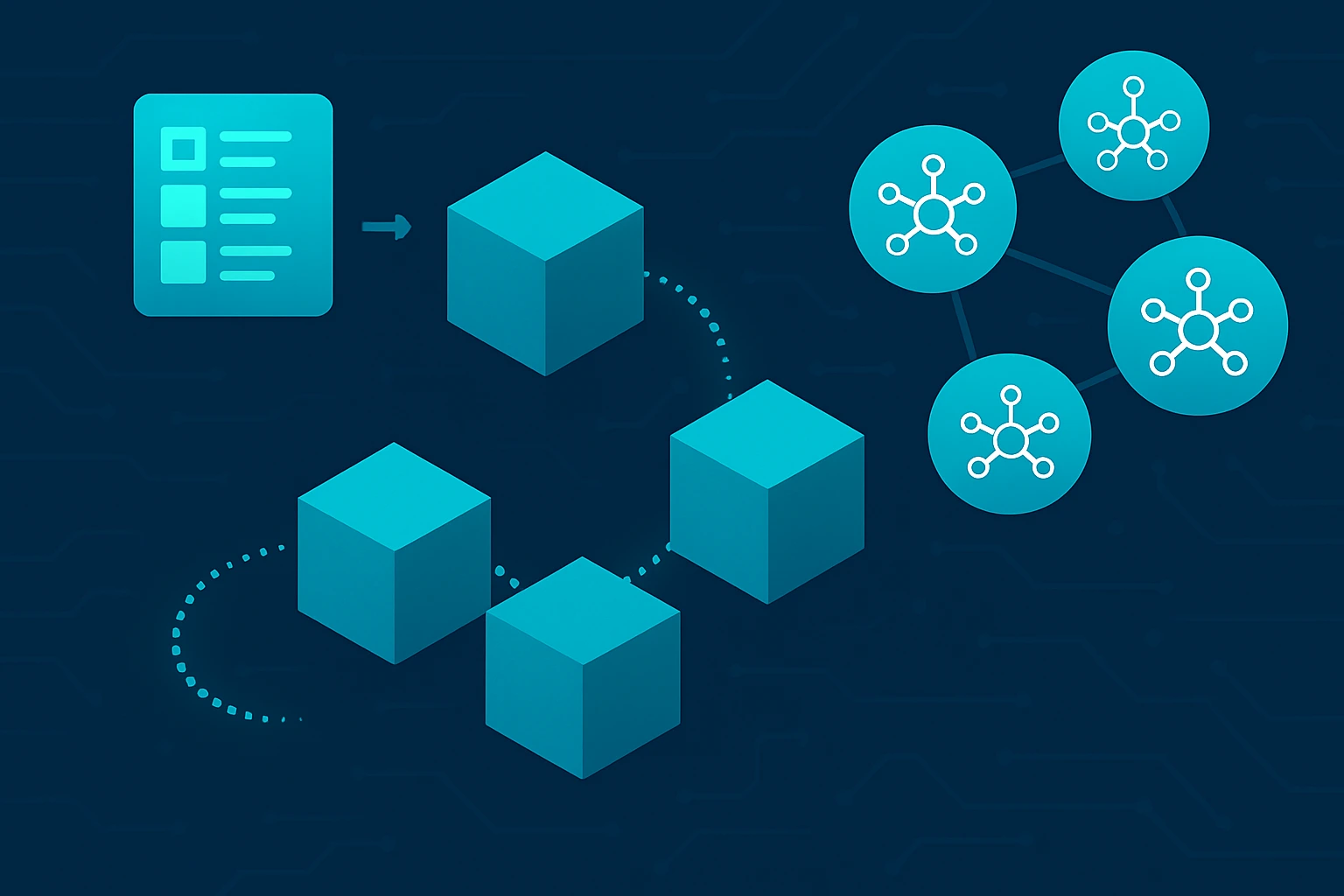

- A blockchain is a shared log (ledger) of transactions maintained by many independent computers, not one central server.

- New entries are packaged into blocks that reference previous blocks, creating an ordered history.

- Participants verify entries and follow consensus (shared rules) to decide which block becomes the next part of the record.

- As more blocks build on top, changing the past becomes increasingly difficult, so history becomes effectively stable.

How Blockchain Works (High-Level)

At a high level, a blockchain works by letting anyone propose changes, having the network verify them, and then recording accepted changes in a shared sequence called blocks.

A simple 4-step flow

Consensus (High-Level)

In a decentralized network, different participants may briefly see different versions of recent history.

Consensus is the set of rules that helps the network converge on one shared version of that history over time, even when multiple blocks or proposals compete.

There is no central vote or controller. Each participant independently follows the same rules, and those rules push the network toward a single shared chain that becomes harder to change as it grows.

What Makes a Blockchain Different from a Regular Database

Core properties

Where Blockchains Are Actually Useful

Blockchains are most useful when you need a shared record across multiple parties who do not want a single administrator.

If you are happy with a single trusted administrator, a traditional database is usually simpler.

Good fits

- Payments and settlement: moving value without relying on one central operator

- Audit trails and provenance: showing when something happened and in what order

- Shared coordination: systems where many participants must verify the same sequence of actions

Trade-offs (High-Level)

Pros

Cons

Where the Idea Came From

The first widely known blockchain design appeared in the Bitcoin whitepaper (2008), which showed that a network of strangers could maintain a shared ledger without a central administrator.

In brief:

- 2008–2009: Bitcoin introduces the first widely used public blockchain.

- 2015: Ethereum expands the idea with programmable applications.

- Today: Blockchains are used wherever multiple parties need the same timeline without one owner.

For beginners, it helps to think of “blockchain” as a way to maintain shared digital history — not as a synonym for hype.

The Mental Model

A blockchain is a system for maintaining a shared history without a central owner. Transactions propose updates, blocks batch and order them, and consensus helps the network converge on one timeline when there are competing proposals.